I’ve been doing a series on words that your banker might use. If you get fluent with them you can talk to your banker like you know what you are doing. It’s just another way to help you get that mortgage you need.

Amortization means ‘causing death’, which seems more like a medical term than something at a bank and although having to go talk to someone at a bank might seem like a fate worse than death for some, it really is a banking term. Each payment you make causes the mortgage to get closer to its end, or death. And who wouldn’t want to take their mortgage and choke it to death?

Loans have different types, the mortgage, or ‘dead pledge’ is often the one you will use in real estate. So many morbid terms. But, in 16th century England, debtors in certain circumstances could be executed. How’s that for morbid? And, it probably had an adverse effect on lenders, because people would be more fearful to take out a loan. You might think that interest rates would have been lower because of that, but the English government had to pass a law to keep rates at 10%.

When you are issued a loan, there is a rate attached to it. Typically, that rate is the annual amount that will accrue, so a loan of $100 at a 10% rate would have $110 owed after a year. But, the bank wants to to be paying down the loan, usually monthly. And so each month, the interest is calculated based on what is left (known as the principal). The monthly rate would be 1/12 of the annual rate. 10% annually would be 0.83% monthly. This is known as monthly compounding, though it could be daily or even continuously, but these are less likely.

Your loan will have an amortization attached to it. This will be the number of months of payments it will take to get to $0 principal. But, because the interest compounds monthly (usually) the amount due goes up a little bit each month and goes down a little bit when you pay the debt service. An amortization of 240 months is the same as 20 years. Some people would call this a 20 year loan, but they are really thinking of more of the term, the time until the loan matures, or needs to be paid off. For your primary residence, the term and amortization will be the same, usually 30 years. For commercial loans, the term is often 5-7 years, which forces the borrower to refinance, and protects the bank from handing out a loan at a low interest rate and making very little money.

There is a calculation that goes in to how much is paid each month. If you work it out for every month of the loan and put it in a table, we call it an amortization schedule. You can create one of these in your favorite spreadsheet if you like math, or you can go over to my favorite calculator at Bankrate.com. Even they mistake term for amortization, just put your amortization number where it says term. They get away with this because most people are residential buyers and the term and amortization are the same for them.

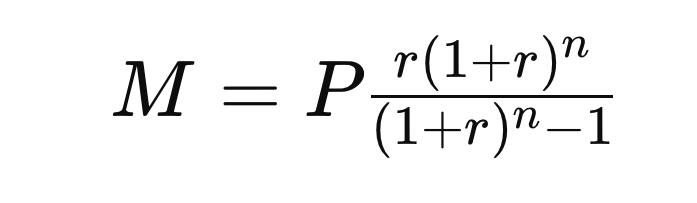

Play around with the amortization schedule. When it is calculated, every monthly payment is the same, except for the last one, which closes out the balance. This is nice for the borrower to know exactly how much will be due every month and to know that it won’t change. Each part of that payment has a principal part and an interest part. Each month the interest part decreases and the principal part increases. The longer you pay, the faster the principal goes down as you are ‘killing’ off your mortgage. If you want to do the math, here is a handy equation from Wikipedia:

- M = Monthly payment

- P = Loan principal (the initial amount borrowed)

- r = Monthly interest rate (annual interest rate divided by 12)

- n = Total number of payments (loan term in years multiplied by 12)

The amortization, then, is the time it will take to pay off the loan when making regular minimum payments. Longer amortization typically means a lower monthly payment, but the bank will charge a higher interest rate usually. Taking a shorter amortization means higher payments, but less interest paid for the amount loaned. This is going to typically be lower than getting the longer amortization and paying more to pay down principal. Make sure you keep this in mind the next time you are getting a loan.