Previously, we talked about why it is so important to calculate your net worth. If you don’t know what I’m talking about, read this post first. And it is very important for you to know this number and to update it at least every six months.

Why Calculate the Net Worth?

- Banks want it. You’ll need this for most of your commercial loans. When you are starting out and buying residential properties in your own name, the bank will look at your personal financials and not usually ask for your net worth. Get bigger and you’ll need one to apply for a loan.

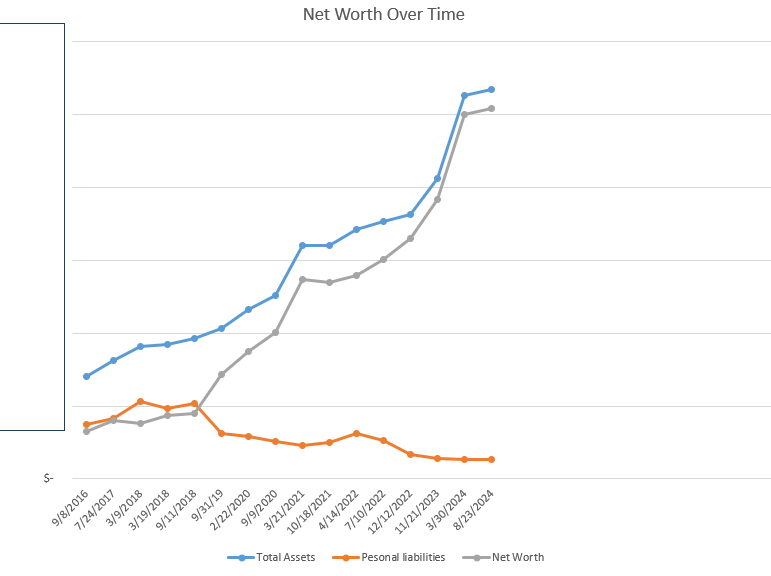

- Monitor how you are doing with your investments. Have a look at this graph I’ve been keeping:

Every time there is a big jump, it’s when I purchased real estate. That’s powerful information to have.

How to Calculate Net Worth

It’s easier than you might think. It’s no more than all of your assets minus your debts. Get out your password manager and start looking through it for all the lenders you use. This will be a pain the first time, but it will get easier.

Income: This is your personal income from salaries/wages, commissions, side businesses, income from dividends, rentals, or child support/alimony.

Expenses: This will take a lot of estimation, but you’ll want to put down big ticket recurring expenses like property tax, insurance, and bills.

Net Income: Subtract expenses from income and put it on this line.

Liabilities: Log on to every one and write down the lender, account number, and amount in a spreadsheet. Also, put today’s date on there so you can keep track. Things that go into debts are: All of your credit cards and their balances, all of your bank loans and their balances (don’t worry about the interest rates), any personal loans you have (for cars or whatever).

Assets: List all the properties you own and your best estimate of the value you would get for selling them now. If you don’t know, you can estimate by taking the property tax value from the tax assessor’s website and multiplying by 1.1 for a rough estimate. Any high-value items like jewelry, vehicles, gold/silver, antiques can be put in here as well. Just use your best estimate of their value but stay conservative. Next, put in the balance of all your bank accounts, retirement accounts, stocks, and life insurance cash values.You’ll be doing a lot of website checking for this one.

Net Worth: Take the assets and subtract the liabilities to arrive at the net worth. Pat yourself on the back for all the work you’ve done to get here.

Make sure you update this every six months. Keep a copy handy and updated for the next time your bank requests it. You’ll look professional and prepared, and put yourself on the best footing for that next loan.